Got losses? Here’s how to use them to cut your tax bill

After the wild ride that was 2022, many crypto investors saw losses - and plenty of them. Fortunately, as we come out of crypto winter, there’s a silver lining for your tax bill. Crypto tax calculator, Koinly, explains the lay of the land.

Crypto investors are starting to see the light at the end of the tunnel after a brutal winter where the market lost an estimated $2 trillion since the all-time highs of 2022. That’s without even factoring the billions in losses from collapsed exchanges, hacks, and other scams. All this to say, if you’ve got losses, you’re not the only one.

But there might just be a glimmer of hope when it comes to your tax bill. That’s why we’ve teamed up with crypto tax calculator Koinly to tell you everything you need to know.

Gains vs. losses

First, you need to understand how capital gains and losses work.

Starting with the obvious, crypto tax varies worldwide - so you should always check the precise rules where you live. Koinly has more than 20 guides on crypto tax around the world to help you.

Generally speaking, most tax offices around the world view crypto as a kind of asset - like a property or stock. Any time you dispose of a property, by selling, swapping, spending, or even gifting it (depending on where you live) - you’ll realize a capital gain or loss.

You’ll pay tax on capital gains, while capital losses can be offset against gains to reduce your tax bill. Let’s take a look at how best to use losses to reduce your tax bill.

Track, harvest & offset losses

There are three steps to using losses to cut your tax bill:

- Track unrealized losses

- Harvest losses

- Offset your losses

1. Tracking unrealized losses

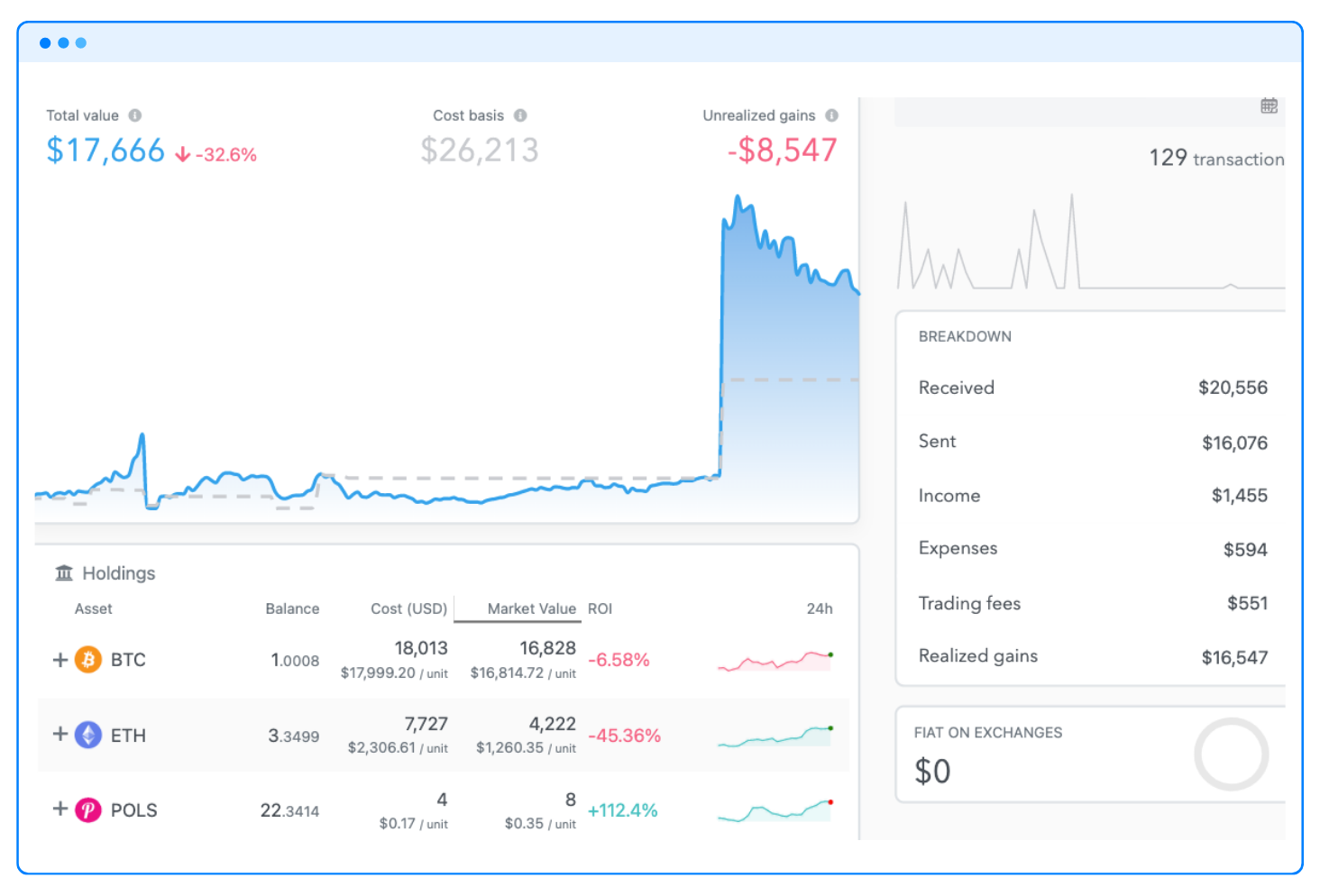

Smart investors track both the good and the bad to help them understand how their entire portfolio is performing.

You don’t need to do this with a spreadsheet either - you can use a crypto portfolio tracker like Koinly to help you track both your overall performance and the performance of your individual assets.

This helps you know where and when to take your profits or cut your losses as your portfolio tracker can track both your realized and unrealized gains and losses.

Once you’ve spotted an unrealized loss, you need to harvest it.

2. Harvesting losses

Once you know where your unrealized losses are, the next step is harvesting them. This part is key because unrealized losses are worthless from a tax perspective. You need to realize your loss by disposing of your asset in order to be able to offset it against your gains.

Generally speaking, you can realize a loss by selling, swapping, or spending your crypto - although some countries also count gifting crypto as a disposal.

Of course, sometimes disposals are easier said than done. There are some scenarios where it's not quite so simple to dispose of your crypto, for example, rug-pulled tokens, illiquid NFTs, funds frozen in exchanges, and losses from theft. Let’s take a quick look at how you may be able to deal with these to realize your loss:

- Rug-pulled tokens: Rug pulls leave you with a token that is effectively worthless, but until you dispose of it it’s an unrealized loss. How you can dispose of your token depends on how illiquid the market is. If you can sell your tokens, even if for virtually nothing, do this. If you can’t, see if you can swap them using a native non-custodial wallet, again, even if this is for another virtually worthless token, this can still help you realize your loss. If neither of these is an option - sending your rug-pulled tokens to a burn address is another way to dispose of them. If you’re outside the US, you may also be able to gift your tokens to realize a loss.

- Illiquid NFTs: Illiquid NFTs present a great tax loss harvesting opportunity - you just need to dispose of them. Like above, the easiest way to do this is to sell your NFT if you can - even if it's for almost nothing. If this isn’t an option, send your NFT to your blockchain’s burn address in order to realize your loss.

- Funds frozen in crypto exchanges: Unfortunately, if you’re one of the millions of investors with funds stuck on now-collapsed exchanges like FTX, Celsius, or Voyager, there’s very little you can do to realize your loss. The best plan here is to sit tight and wait for bankruptcy proceedings to conclude. Try not to lose hope though, many investors are finally starting the claims process as part of bankruptcy proceedings and will hopefully see at least some of their funds returned soon.

- Losses from theft: For US investors… it’s bad news. The IRS says theft is not a capital loss unless it's related to a federal disaster. For other investors worldwide though, many countries like Australia, Canada, and the UK allow investors to make a capital loss claim due to theft, provided they have enough proof.

3. Offset losses

Depending on where you live, you’ll have to follow slightly different rules when offsetting your capital losses. But here are the basics:

- For most countries, there’s no limit to the number of losses you can offset against gains, except in countries where you only pay tax on a certain percentage of your gains. For example, in Canada, as you only pay tax on half of any capital gain, you can similarly only offset half of any loss.

- Got no gains? You can usually carry losses forward to offset against gains in the future - but you may need to register these with your tax office in order to do this.

- Generally, you can only offset losses against gains of a similar nature - so for example, you can’t usually offset losses against income. Although there are a couple of exceptions to this, like the IRS allows taxpayers to offset $3,000 in capital losses against ordinary income each year.

- Thinking of just selling all your crypto at a loss and buying it back? Most tax offices have rules to stop you from doing this known as wash sale rules. Wash sale rules vary from country to country, but they all prevent investors from selling an asset at a loss and re-acquiring that same asset back in a short time frame. If you have a wash sale, you can’t offset this loss against gains. Although there are some exceptions to this - for example, in the US, the wash sale rule doesn’t yet apply to crypto. You can learn more in Koinly’s crypto tax loss harvesting guide.

Reduce your tax bill with our partner Koinly

Our crypto tax partner, Koinly, helps you track your crypto portfolio performance - making it easy to track, harvest and realize your losses in order to cut your tax bill.

In even better news, Koinly helps you calculate your crypto tax liability and generate a range of reports for tax offices around the world.

Get an exclusive 50% discount on Koinly crypto tax reports when you sign up to Koinly using code NICEHASH

Disclosure

The information on this website is for general information only. It should not be taken as constituting professional advice from Koinly. Koinly is not a financial adviser or registered tax agent. You should consider seeking independent legal, financial, taxation or other advice to check how the website information relates to your unique circumstances. Koinly is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by use of this website.