Navigating the Fourth Bitcoin Halving: Economic Impacts and Innovations

Since 2010, the Federal Reserve has increased M2 money supply by $12.3 trillion. This immense ballooning of available liquidity introduced much noise into the monetary system. Because money is a unit of information for exchanging value, such dilution erodes the value of money.

This effect is known as inflation. But what happens when a new asset pops up to counter such a monetary system?

This is the story of Bitcoin and its halving mechanism. Unlike the dollar with unlimited and arbitrary dilution, Bitcoin is limited to 21 million units, further denominated into satoshis (sats). To properly introduce this novel asset, it has to be made scarce not only by its 21 million hard cap, but also by its liquidity inflow.

Bitcoin’s halving is just such a disinflationary mechanism, serving as a dam that decreases the rate of newly mined coins. At approximately 210,000 mined blocks, or four years, Bitcoin’s hard-coded protocol cuts in half the reward miners receive for securing the network and facilitating the transfer of wealth.

This means that Bitcoin’s first (Genesis) block yielded 50 BTC miner reward as the first ever BTC supply pool in January 2009. That reward was cut three times since:

- In 2012 from 50 to 25 BTC

- In 2016 from 25 to 12.5 BTC

- In 2020 from 12.5 to 6.25 BTC

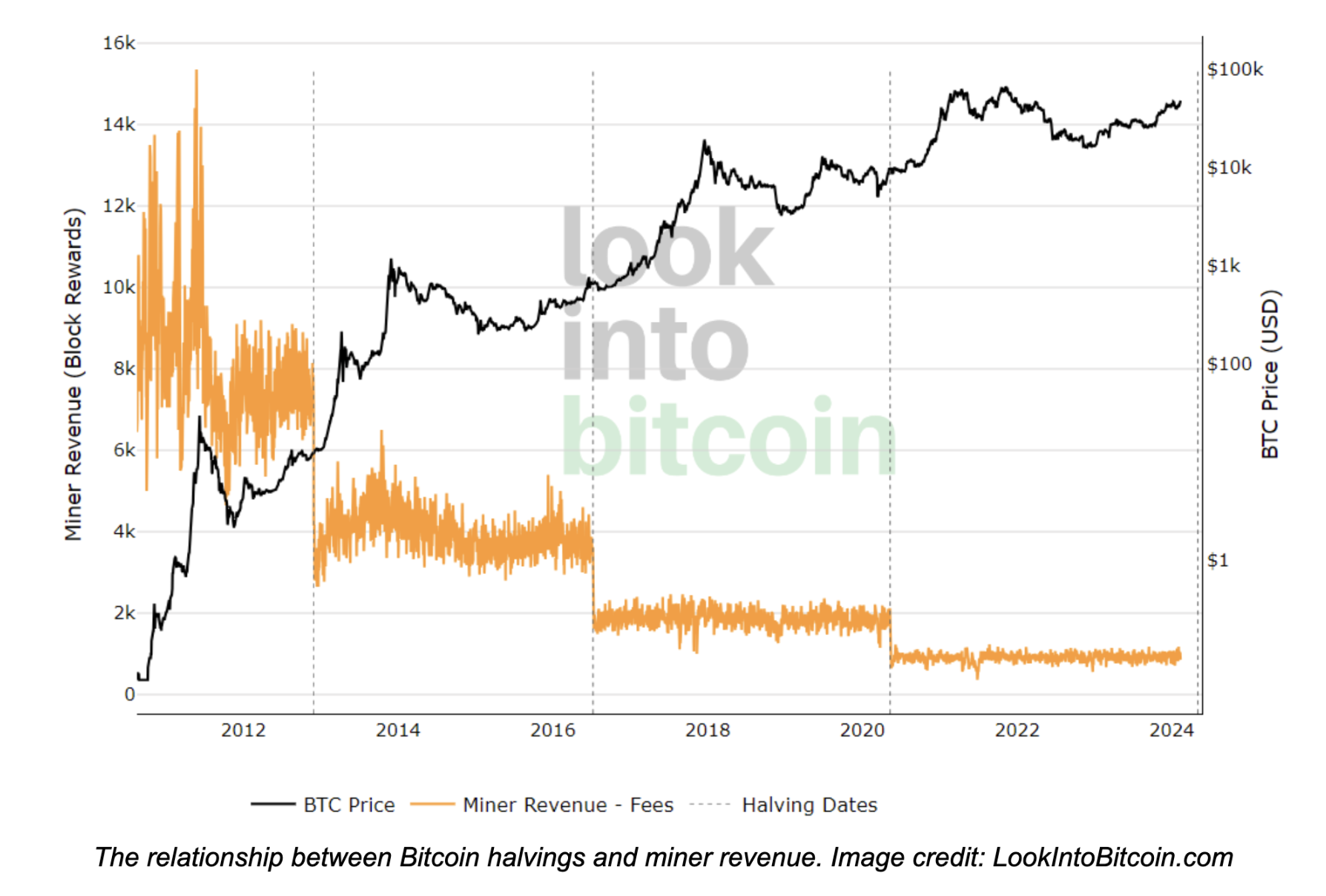

In turn, Bitcoin’s inflation rate dropped from triple-digit range in 2009 to present 1.74%. And because Bitcoin’s limited supply creates scarcity, BTC price is inversely proportional to its inflation rate as seen on the chart below.

At 93.46% mined circulating supply out of possible 21 million BTC, Bitcoin’s present inflation rate of 1.74% is heading into another cut in April 2024, from 6.25 to 3.125 BTC miner reward.

With rewards so reduced, this poses a shift in incentives for miners. For Bitcoin holders, what are the implications?

Historical Context and the Changing Landscape of Bitcoin Mining

For a new asset to counter the Federal Reserve, or any other central bank, it has to meet two key requirements to be perceived as a worthy substitute:

- It must eliminate central authority that could tamper with its supply.

- It must prevent double-spending, i.e., falsifying transactions by spending the same BTC more than once.

Bitcoin reached these requirements by combining incentives with the difficulty of mining new bitcoins. Without an imposed barrier of entry, the Bitcoin network grounded itself in the proof-of-work algorithm. It allows Bitcoin’s digital nature to become physicalized.

In other words, miners must exert significant computing power, which requires hard assets and energy, to solve complex mathematical equations as they validate transactions. When such problems are solved (proofed), miners receive bitcoins for their expenditures.

In turn, malicious actors are kept out of the game because they cannot overcome the combined power of Bitcoin’s computing network securing the transaction ledger. By the same token, Bitcoin gains validity as sound money, simultaneously digital and hard.

This is the elegant core of Bitcoin’s design, as it combines incentives with blockchain technology. However, as Bitcoin halvings decrease the inflation rate by cutting mining rewards, they also cut the mining revenue in half as well.

Prior to the first halving in 2012, when Bitcoin price ranged between $3 - $20, miner block rewards were at a minimal level of $7,000. In the present cycle, when Bitcoin price is above $45,000, miner block rewards are in the $1,000 range.

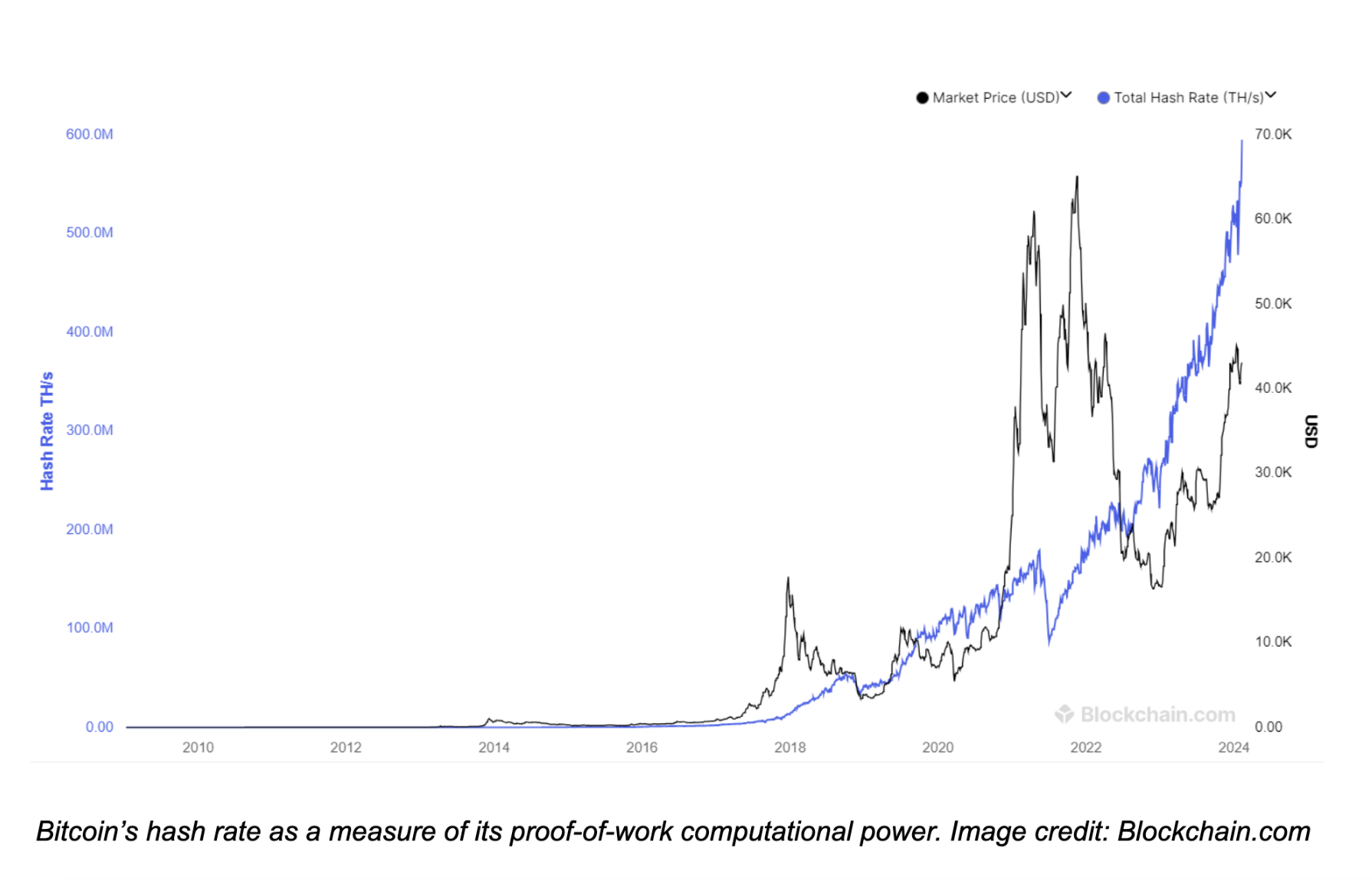

At a superficial glance, one could think that such diminishing rewards would degrade Bitcoin’s incentive framework and the value of bitcoins in turn. Yet, the combined computing power of the network, expressed as hash rate, has only increased, reaching a record 595 million TH/s.

Bar none, this translates to Bitcoin having the most powerful computing network in the world, further bolstering Bitcoin’s perception as sound money, which then feeds into Bitcoin’s higher price.

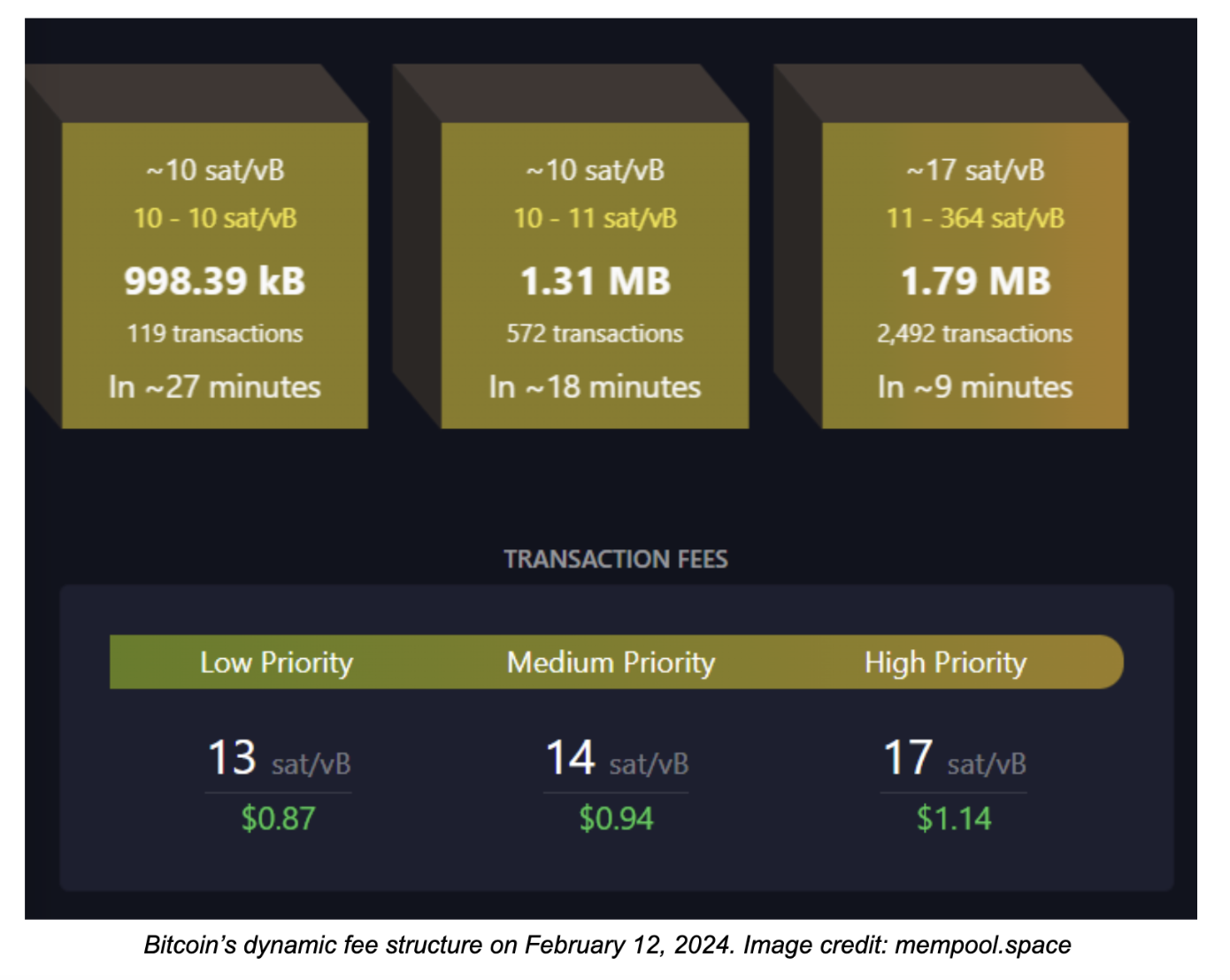

To balance the reduction in block rewards, Bitcoin miners then resort to revenue from transaction fees. Those who wish to process their transactions faster select from a fee tier. Their price depends on the traffic load on a given day.

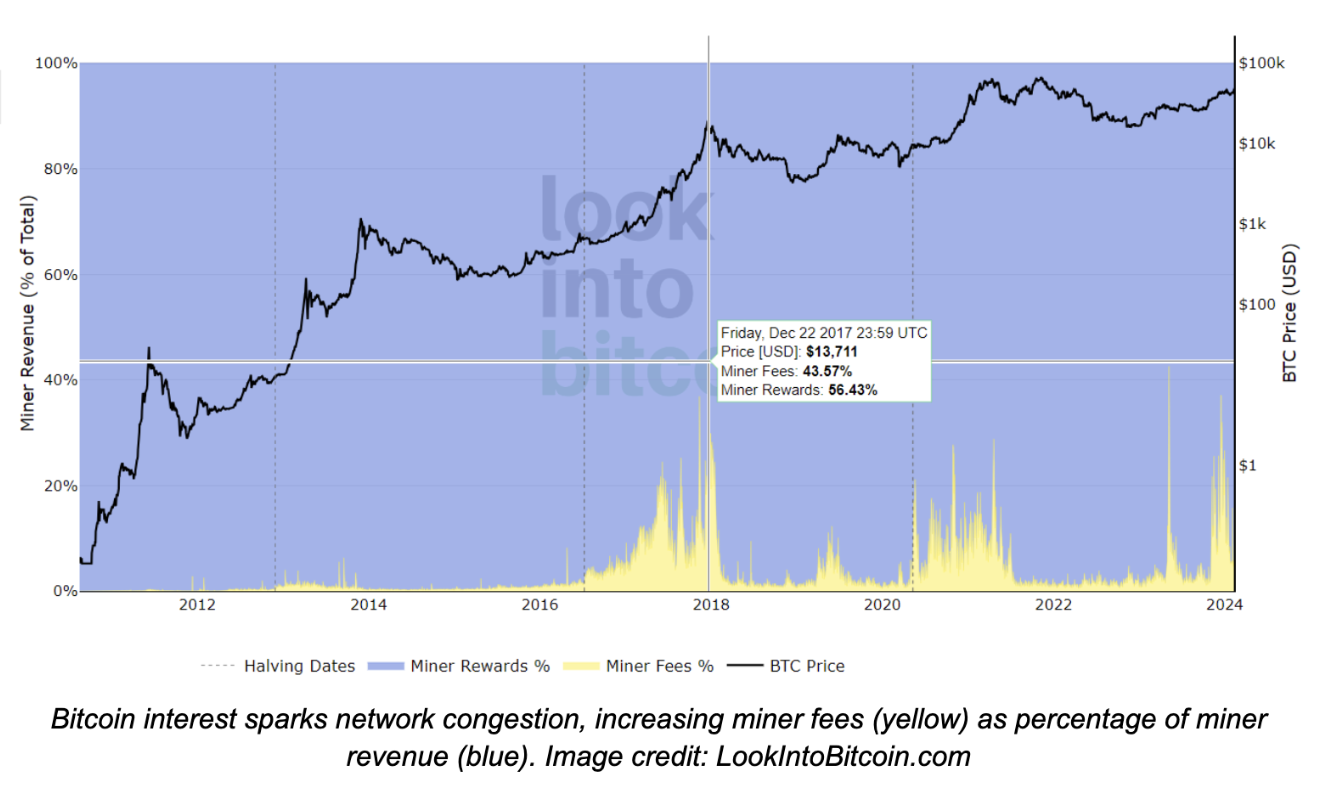

Just like any other computer network, Bitcoin’s has a limited bandwidth. With an average block size of 1.6 MB, only so many transactions can fit into each block. Consequently, during hype events such as positive news or halvings, the increase in network traffic yields a higher percentage of miner revenue coming from fees vs block rewards.

Case in point, the sudden spike in Bitcoin price, starting the year 2017 at under $1,000, only to go nearly $20,000 by December, marked the highest ratio of 43.57% vs 56.43% in favor of fees vs block rewards for miner revenue.

Likewise, when the US regional banking crisis renewed Bitcoin interest, miner revenue from fees increased to 42.60% by May 2023. Because of the aforementioned disinflationary mechanism, Bitcoin halvings themselves represent Bitcoin hype events.

The psychological impact of money erosion is best exemplified with the need to constantly reinvest and reallocate. Even more so with the help of various trading platforms for short selling. Within a year of each halving, BTC price increased drastically, but at lower rates each time:

- 1st halving on November 28, 2012, ~8,300% price boost

- 2nd halving on July 9, 2016, ~2,600% price boost

- 3rd halving on May 11, 2020, ~600% price boost

At the end of the day, Bitcoin’s scarcity and price appreciation had historically offset the reduced block rewards for miners. Ahead of Bitcoin’s 4th halving in April 2024, miners face new challenges and opportunities.

Challenges and Opportunities in the Upcoming Halving

After the 4th Bitcoin halving, Bitcoin’s inflation rate will drop under 1%. As the BTC price went up, the growing competition between Bitcoin mining companies has steadily increased the mining difficulty.

This mechanism automatically adjusts every 2,016 blocks, or two weeks, as a stabilizing measure to maintain a consistent block production rate every 10 minutes. In other words, whether miners are unplugging or plugging into the Bitcoin mining network, puzzle difficulty decreases or increases respectively.

The difficulty mining mechanism is one of Bitcoin’s core embedded features to secure the network and repel a 51% attack. In practice, this means that mining companies such as Marathon, Riot or Hut 8, must improve their cost-effectiveness, reinvest in better rigs and better cooling solutions while finding cheaper electricity sources.

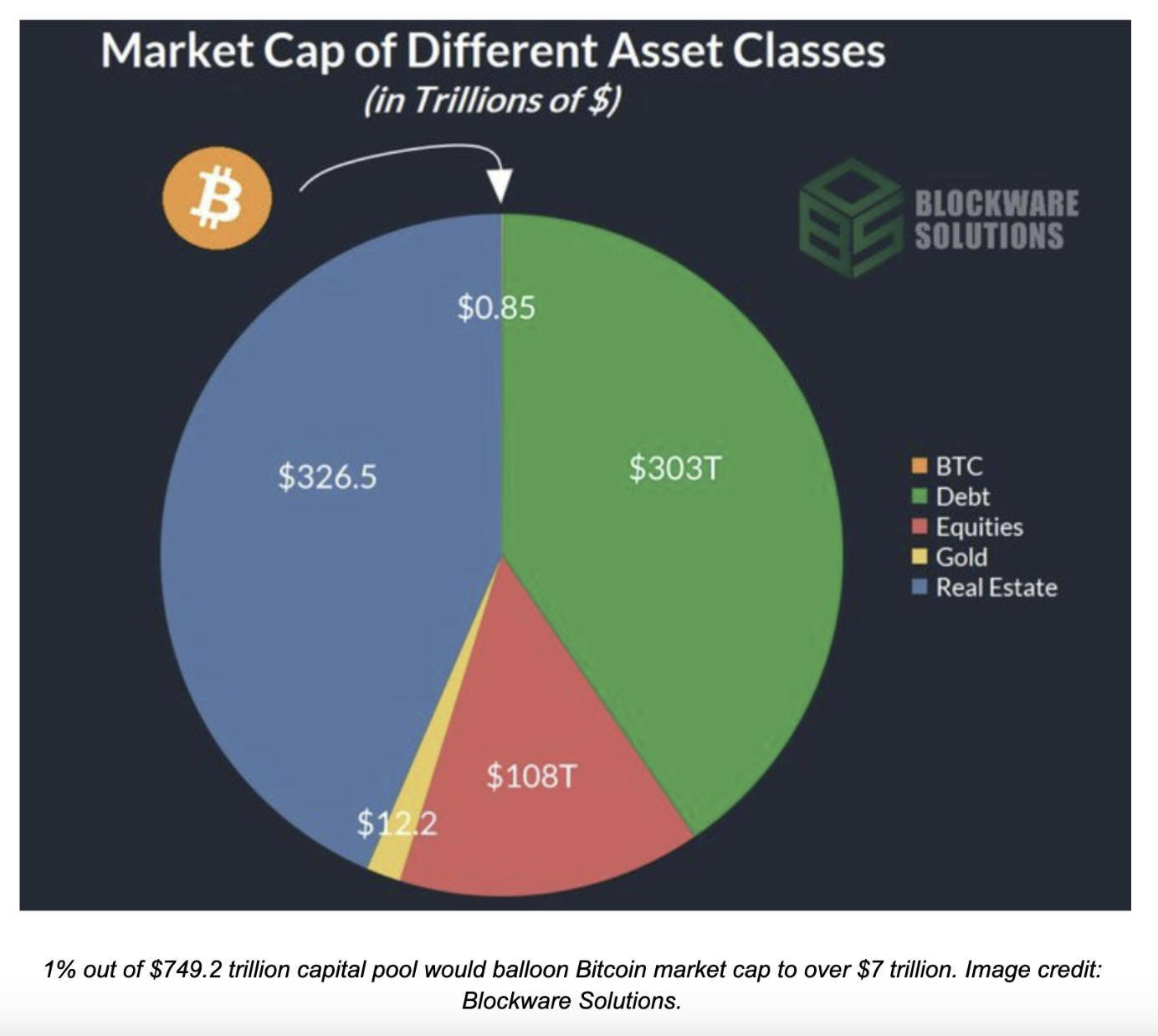

Following Bitcoin ETF approvals, more BTC price boosting is expected to offset these costs. The ETF approvals represent a milestone in BTC exposure, opening capital gateways from institutional investors. Even if various funds and financial advisors start allocating 1% of their portfolios into Bitcoin, the resulting buying pressure could boost BTC price up to $400,000.

By the end of 2024, Standard Chartered analysts forecasted an inflow of $50 billion to $100 billion into Bitcoin ETFs. Moreover, a new miner revenue source could become more consistent.

The New Factor - Ordinals and Market Dynamics

Courtesy of Bitcoin’s Taproot upgrade in November 2021, building up from the SegWit upgrade in August 2017, a new class of assets was made possible on the Bitcoin network. By upgrading Bitcoin’s scripting capabilities, network users could attach metadata to transactions, eventually leading to Bitcoin Ordinals and inscriptions.

While Bitcoin Ordinals attach a unique number to each satoshi, as the smallest Bitcoin unit, in a specific order, inscriptions attach metadata to a specific satoshi akin to non-fungible tokens (NFTs). This resulted in a wide range of digital collectibles. Additionally, this technology could facilitate the use of electronic signatures for authenticating transactions and documents securely on the blockchain, further enhancing Bitcoin's utility by allowing for the minting of critical documents with verified signatures, secured by the world’s most powerful network.

The Ordinals protocol even allows users to create BRC-20 tokens as a new fungible token standard to represent digital assets similar to ERC-20 on the Ethereum blockchain. Although still experimental, they could range from stablecoins and utility tokens to synthetic representations of other cryptocurrencies.

Percentage wise, non-ordinal BTC transactions still dominate miner revenue with occasional experimental spurts.

![]()

Cumulatively, the Bitcoin network now hosts nearly 60 million ordinals, with total BRC-20 fees paid worth 4,741.18 BTC. For comparison, global Bitcoin miners mine on average 900 BTC daily.

The creator of the Ordinals protocol, Casey Rodarmor, also created the Rodarmor Rarity Index. Contrary to popular belief, no longer are all satoshis (sats) created equal as the smallest BTC units. After each halving, the first mined sats are considered “epic sats”.

Such rare sats include those that are mined after each difficulty adjustment period. Altogether, the supply of these rare sats is scarce within the already scarce BTC supply:

- Mythic - the first sat from the Genesis block

- Legendary - every six halving events (24 years)

- Epic - every halving event (4 years)

- Rare - every difficulty adjustment period (2 weeks), presently numbering 3,437

In other words, the emergence of sats ratings presents miners with incentives to claim them. They would do so by checking Unspent Transaction Output (UTXO) of their wallets, by connecting the wallet to marketplaces such as Magisat for scanning.

If such applications become popular, Bitcoin miners could boost their revenue with more transaction fees coming from trading and collecting rare sats. Likewise, if rare sats gain popularity, BTC price itself could rise, leading to higher BTC demand that further increases miner revenue.

Conclusion

Central banks have yet to achieve their ideal inflation target of 2% while Bitcoin’s 4th halving is heading to place BTC issuance under the 1% range. Given governments’ propensity to spend more than they collect in revenue, the fiat money’s fate seems to be sealed - devaluation.

Bitcoin miners make the core of the alternative monetary system, predictable, decentralized and secure. Even with diminishing block reward returns after the 4th halving, their revenue is tied to the elegant feedback loop:

provide limited sound money <-> the value of sound money goes up

After the Bitcoin ETF approvals, the institutional buying pressure to allocate into sound money is likely to rise. This is another feedback loop, equally stemming from the power of Bitcoin’s computing network and its incentive framework.