Tendencias en criptomonedas para 2023: Hacia dónde se dirige el sector

El mercado de criptomonedas avanza en 2023 a toda fuerza.

Mientras que Bitcoin sube un +40%, altcoins como Tezos (XTZ) y Aptos (APT) se impulsan aún más, un +60% y un +400% respectivamente, basándose en su propia dinámica anticipatoria.

Independientemente de si esta tendencia continúa, marca un importante desprendimiento psicológico del peor año en cripto.

Tras las lecciones de 2022 y las innumerables quiebras, que las criptomonedas se vuelvan alcistas dependerá en gran medida de la política monetaria de la Reserva Federal, las condiciones macroeconómicas y la reacción del mercado bursátil.

Sin embargo, hay algunas criptotendencias en 2023 que son más claras que otras. Veamos tres de ellas.

Mayor escrutinio regulatorio

Ya sea para bien o para mal, el panorama legal de EE.UU. ha estado en gran medida desprovisto de regulaciones sobre criptomonedas en términos de leyes reales. En su lugar, las agencias reguladoras, como la SEC y FinCEN, han emitido un mosaico de reglamentos y directrices. Esta falta de leyes federales exhaustivas ha llevado tanto a las empresas como a los particulares del sector de las criptomonedas a un estado de incertidumbre.

Predominantemente, la SEC ha quedado a cargo del vacío legislativo. La Comisión lo ha hecho:

- Propuestas de modificación de la normativa vigente de la SEC en 2019 para permitir a las empresas recaudar fondos a través de ICO (Initial Coin Offerings).

- Demandadas múltiples personas y empresas por realizar ICO ilegales y estafar a inversores.

- Comenzó a revisar las solicitudes de ETF (fondos cotizados en bolsa) de Bitcoin, sin que hasta la fecha se haya aprobado ni una sola (la primera fue presentada allá por 2013 por los gemelos Winklevoss).

- Publicó directrices en 2020 que aclaran cuándo un activo digital puede considerarse un valor con arreglo a la legislación estadounidense.

Este último punto es el que puede tener mayores repercusiones. La SEC utilizó la "Prueba Howey" para determinar si una criptomoneda podía ser categorizada como un contrato de inversión - un valor. Si un activo digital se lanzó con la expectativa de obtener beneficios derivados del esfuerzo de otros, muy bien podría serlo a ojos de la SEC.

Esto se aplicaría probablemente a todas y cada una de las criptomonedas excepto Bitcoin y Litecoin, y posiblemente Ethereum, según varios comisionados de la SEC.

Dejado a sus propios dispositivos reguladores, tal escenario aún tiene que ser determinado por un precedente legal en el caso SEC vs. Ripple Labs. Si la SEC gana, afectaría a la forma en que se compran y venden las criptomonedas, así como al funcionamiento de las empresas del sector.

La gran mayoría de los criptoproyectos tendrían entonces que cumplir las leyes y reglamentos sobre valores:

- Registrar sus ofertas en la SEC, lo que lleva mucho tiempo y es muy costoso.

- Negociación limitada, ya que los valores están sujetos a más restricciones, lo que limitaría la base potencial de inversores para los criptoproyectos.

- El aumento de los costes legales y de cumplimiento de la nueva normativa probablemente provocaría un éxodo de criptomonedas de Estados Unidos.

A su vez, estas restricciones aumentarían la protección de los inversores y, al mismo tiempo, cortarían el aire de innovación por el que es conocido el criptoespacio.

Un avance rápido hasta principios de 2023, después de un año de colapsos, quiebras e inversores que pierden miles de millones en el espacio de las criptomonedas.

En cuanto a los decretos ejecutivos, la Casa Blanca publicó una hoja de ruta sobre criptomonedas el 27 de enero. El encuadre parte de una perspectiva negativa, ya que el "Mapa de ruta para mitigar los riesgos de las criptomonedas”.

Citando la implosión de la stablecoin UST de Terra y el desplome de FTX, el gobierno de Biden no ve con buenos ojos el criptoespacio. Cualquier posible acción legislativa por parte del Congreso debería "no dar luz verde a las instituciones dominantes, como los fondos de pensiones, para que se lancen de cabeza a los mercados de criptomonedas".

Hacerlo sería "un grave error", según la Casa Blanca. Lo más probable es que la Administración Biden favorezca una legislación que, a su vez, favorezca a las instituciones financieras establecidas. Sin ir más lejos, antiguos empleados de Goldman Sachs y otros asociados jugaron un papel importante en la formación del equipo de Biden en 2020.

Del mismo modo, Goldman Sachs ha revelado sus planes de realizar una compra multimillonaria de cripto descuentos tras el colapso de FTX, después de haber invertido ya en 11 startups de criptomonedas. Y no son los únicos con esa perspectiva.

"Los clientes han perdido la confianza en algunas de las empresas más jóvenes del sector que se dedican exclusivamente al cripto, y buscan contrapartes más fiables."

-Mark Bruce, Consejero Delegado de Britannia Financial Group a Reuters

Regardless, what’s clear is that the US Congress is full of representatives calling on new laws to protect investors. Regulatory agencies are generally reactive as opposed to proactive - and it’s likely that they’ll react to 2022 with incoming regulations in 2023.

Securities Tokenization

Bitcoin played a crucial role in establishing digital assets as a legitimate concept in the mainstream consciousness. Alongside this milestone task, Bitcoin also showcased the advantages of blockchain technology itself. Because blockchain enables records to be immutable, this opened the door to trusted 24/7 settlements without intermediaries.

The next evolutionary step is the tokenization of securities. As such, security tokens are digital representations of real-world assets: bonds, stocks, real estate or even artwork, if sold as an investment. Ownership of these assets is recorded on a blockchain ledger as a token, making it more secure, transferable, and accessible to a wider range of investors.

In this intersection between blockchain tech and traditionally regulated securities, we can look forward to a 24/7 marketplace for securities, drastically increasing liquidity and accessibility. At least, that is what Larry Fink foresees as the CEO of BackRock, the world’s largest asset manager with $10 trillion AuM:

“I believe the next generation for markets… for securities, will be tokenization of securities.”

-Larry Fink, CEO of BlackRock

Why is that important?

Following the GameStop/AMC short squeeze in January 2021, we have seen the underbelly of stock trading. It is a fragile labyrinth that consists of multiple intermediary institutions. In turn, when the trading volume is high, it can result in over 1 million GME shares failing-to-deliver (FTD).

That’s because the US stock market relies on a two-day trade settlement period (T+2), from the broker (e.g. Robinhood) to the market maker (e.g. Citadel Securities) and into the clearinghouse (DTCC). If tokenized, such trades would execute on a single, secure blockchain network in real-time, 24/7.

“There is no reason why the greatest financial system the world has ever seen cannot settle trades in real time. Doing so would greatly mitigate the risk that such processing poses.”

-Vlad Tenev, CEO of Robinhood

Consequently, with the settlement time near-instant on a blockchain, the risk is reduced. And as more trades can be executed in a shorter time frame, eliminating trade-settlement lag, this leads to better price discovery and increased market liquidity.

When CBDCs are deployed, we will likely see this kind of enhanced efficiency in the forex markets as well. Presently, because traditional banks serve as intermediaries, traditional forex brokers also deal with a multi-day trade-settlement lag.

More GameFi, NFTs and Options Trading

Coming full circle, why is it that Aptos (APT) is up by over +400% this year? Outside of the fundamentals of being a novel and fast proof-of-stake L1 chain, much of that has been driven by NFT trading. In turn, this increased the overall speculation buzz and APT demand.

As Mohammad Shaikh, co-founder of Aptos Labs explains, non-fungible tokens (NFTs) should go beyond mere collectibles in 2023:

“NFTs should have an opportunity to live in things like games, social platforms that might be out there, where you share what you own, why you own it and really connect with the community.”

In other words, just like tokenized securities bridge traditional finance and blockchain, NFTs provide agnostic ownership tokenization. This extends from GameFi to even car titles as NFTs, which is presently being implemented by California DMV on a privately instanced Tezos blockchain.

On one end, GameFi is a subset of the metaverse, as people use portable digital assets to engage in gamified financial tools, like yield farming, borrowing and lending. But zoomed out, metaverse revolves around portable digital assets used across multiple virtual environments in a seamless manner.

It’s this blockchain interoperability that creates the “meta”. In 2023, we will see multiple Web3 gaming ecosystems come online, including the newly launched MetaPixel for Aptos, from the renowned Korean NPIXEL, the creators of Gran Saga that is soon coming as Gran Saga Unlimited on Aptos.

2022 may have been overflowing with bankruptcies, but it bears keeping in mind that the ‘metaverse’ received $120 billion in just the first half of the year, according to a McKinsey report.

Even JPMorgan published hyper-bullish metaverse forecasts:

“The metaverse will likely infiltrate every sector in some way in the coming years, with the market opportunity estimated at over $1 trillion in yearly revenues.”

In 2023 and the following year, these investment seeds are bound to sprout into metaverse trees. However, we have yet to see a ‘killer’ app or game. Until that happens, institutional traders will increasingly use crypto options trading to hedge their bets.

Increased Crypto Options Trading

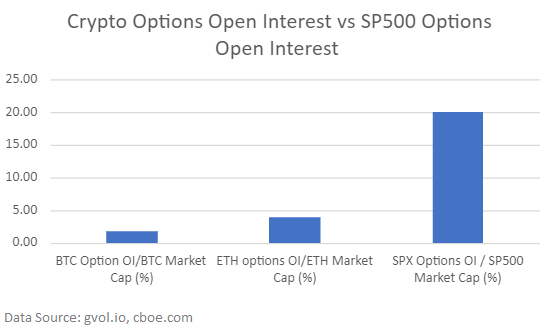

During the bear market in August, speculation on Ethereum's Merge was all the rage, even outpacing Bitcoin open interest. However, given how young the crypto industry is, Bitcoin’s slight 2% open interest was impressive compared to traditional options on stocks at 20% of S & P 500’s market cap.

At the time, Enhanced Digital Group (EDG) forecasted this as the beginning of growth and popularity in crypto options trading.

“When you think of all the other [S & P 500]-like products including ETFs, SP Minis, etc., you can see that bitcoin options have multifold growth ahead of it,”

-EDG’s Marcin Maksymiuk

In 2020, amid Covid-19 shutdowns, options trading became incredibly popular among a younger, retail-oriented audience. This trend continued into 2021, which saw a 35% increase YoY in options trading, fueled by retail. From easy to use trading apps such as Robinhood and the popularity of options alerts to help guide newer investors, popularity in options trading skyrocketed among a newer, younger demographic - the same demographic that actively trades cryptocurrencies as well.

Options trading has slowed down since then - as all markets have - but interest in crypto options is starting to return.

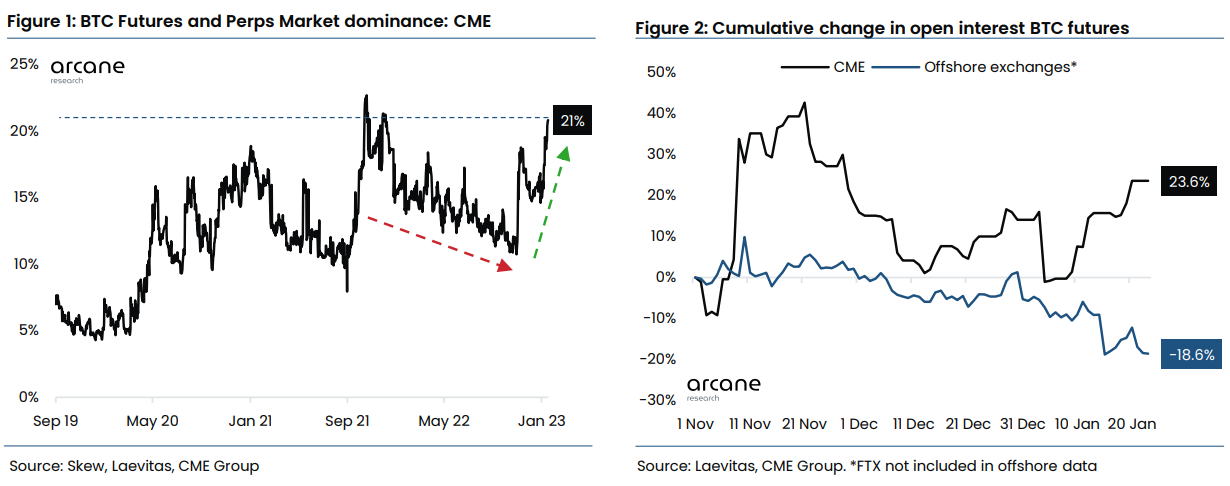

Nearing the end of January, time has proven Marcin correct. Open interest on CME Bitcoin futures rose to a near-record high of 21%, according to Arcane Research. As before, more institutional investors jumped in betting on Bitcoin price moves.

With the likelihood of Bitcoin being deemed as the only top commodity, amid an ocean of crypto securities, we could very well see this reflected further in the crypto derivatives market.